Cuba’s Economy: A Current Evaluation and Several Necessary Proposals

Introduction

In academic forums and in various publications, politicians, social scientists and readers in general, both in and out of Cuba, have noted that the economic well-being enjoyed by the Cuban people in the early 80s was severely impacted by the economic crisis of the 1990s. But it is clear to even the most skeptical of observers that the worsening of conditions was attributable not only to external factors, such as the breakup of the international socialist system, the tightening of the US blockade, and the worldwide economic crisis suffered by underdeveloped countries, but also to internal factors that kept the country from fully realizing its material and human potential.

In 2009, Cuba finds itself in the midst of a new economic crisis, in which it maintains high import rates due to longstanding structural problems in agrarian policy that have resulted in a high dependence on food imports. Likewise, although to a lesser extent, energy needs are very high and production requires many intermediate inputs. This is added to low efficiency and productivity in both industry and agriculture, and diminished financial liquidity in hard currency.

The institutional reforms of the mid-90s led citizens to diversify their sources of income. The market's growing role in generating income, as well as the unique strategies devised by the people, led to a gradual social differentiation that persists despite various measures implemented under the auspices of the "Battle of Ideas," which was basically a set of government programs aimed at halting the deterioration of social indicators: education, health, culture, etc. The so-called "Battle of Ideas" called for large centralized investment projects that focused on the building and repair of schools, hospitals and homes. Another component was as a huge energy conservation plan that included the purchase of domestic appliances for equitable distribution to the public.

Problems persisting many years after the onset of the economic crisis called the "Special Period,” necessarily led to giving priority to addressing the social inequalities engendered during that period. Although it is evident that the country has tried to implement necessary and profound economic changes at the lowest possible social cost, there is a disparity between the pace of change and the urgency of human need.

It is therefore necessary to analyze the state of the Cuban economy through a set of indicators that reveal the current condition of the country and the well-being of its citizens in an effort to gain an understanding of the challenges facing the country.

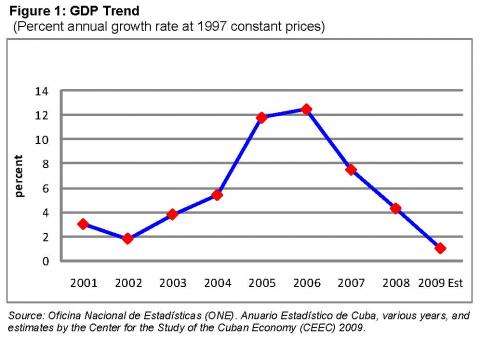

1. Gross Domestic Product (GDP) Growth

The Cuban economy experienced a fluctuating but strong economic growth rate from 2001 to 2007, with an impressive 7.5% average rise in the gross domestic product (GDP) at constant 1997 prices. From 2001 to 2003 growth was only 2.9% per year, but 2004 to 2007 saw annual averages of 9.3%, influenced by the new methodology for calculating the GDP,1 the surge in exporting professional services, and government spending on priority programs. Already in 2008 and 2009 there was a significant dip in economic growth, prompting the government in 2009 to impose a new economic adjustment plan, with negative consequences for the economic well-being of the population.

Predictions suggest that Cuba’s drop in GDP will continue in 2009 and may even become more acute, resulting in the first negative growth-rate in 16 years.

The island's economy has been subject to a series of external shocks, which have severely complicated its operation: a drastic reduction in terms of trade (-38% in 2008), caused mainly by rising oil and food prices and the falling price of nickel, three hurricanes in 2008 costing around US$10 billion, and, more recently, the global financial crisis.

However, the deceleration of the GDP should not be attributed solely to external factors. There are internal structural constraints that have worked against sustaining high growth rates.

Figure 2 shows the GDP trend along with two of the macroeconomic indicators that largely explain it: exports of goods and services, and investments. Exports provide the foreign currency to pay for imports, and thus help to relax the restrictions on balance of payments flows.2 Investments provide capital accumulation, essential for sustaining economic growth in the medium and long term. Figure 2 also illustrates that the strong GDP growth of 2004-06 – with an annual average of 9.6% – was accompanied by an expansion of exports and investment, with rates averaging over 20%. In those years, the Cuban economy began to feel the benefits of agreements with Venezuela and of the boom in the export of professional and technical services, especially healthcare-related. In contrast, during the 2007-08 period, exports and even more so investment slowed, resulting in a deceleration of GDP growth.

The following are some of the structural factors that have influenced the slowdown in exports, in investment and, ultimately, in the Gross Domestic Product:

-- Lag in agriculture and industry not compensated for by the expansion of services.

-- Little diversity in foreign trade. The balance of payments equilibrium depends on the export of professional services to Venezuela.

-- Low multiplier effect of exporting professional services.

-- Low productivity persistent in much of the state enterprise sector. There have been no structural reforms sufficient to change that.

These factors are interrelated and result in a growth pattern that since 2004 has rested on the export of professional services. Furthermore, they act on an economy with a small domestic market that, consequently, is extremely vulnerable and dependent on imports, and which has to cope with a costly economic blockade that, in financial terms, has intensified over the last five years.

The agreements contained in the Bolivarian Alternative for the Peoples of our America (ALBA) and in particular the opportunity to earn outside income from the export of professional services has had an undeniable and substantial impact on the Cuba’s balance of payments and GDP growth since 2004. These revenues are ongoing today and provide some level of security in a time of global economic crisis. The problem is that these exports have begun to slow down and no substitute has been identified in other sectors of the economy, all of which have trailed behind with very low productivity.

Industry and agriculture have not been able to match the expansion of professional services. The export of professional services is not linked to and does not have the multiplier effect on the domestic economy that the sugar and tourism industries have for example. Those industries have driven growth in previous decades. On average, sugar exports and tourism services have stagnated in the last five years, affecting the diversification and sustainability of export growth rates.

In summary, the growth model based on the export of professional services shows signs of structural weakness and exhaustion, manifested in less availability of foreign currency, greater relative scarcity of resources for investment projects and, finally, a deceleration trend in the GDP.

2. Main Sectors

The GDP structure of 2008 shows an accelerated decrease in the relative importance of the agriculture, construction and transportation sectors and highlights a significant increase in services accounting for 76% of the GDP.

The Cuban State’s allocation of the GDP reflects the priority that it has accorded to social programs within its overall development strategy. Nevertheless, while gross fixed capital formation was 60% greater in 2006 than in 2001, its share of total spending has decreased to less than 10% of GDP, in contrast to 1990 when it reached over 30%.

The Cuban economy has been adversely impacted by the context in which it has had to develop, such as severe droughts, the scourge of violent hurricanes, the power generation crisis, and the escalation of US pressure on the country, along with the global economic crisis that began to be strongly felt by mid-2008. In 2009 structural problems persist in the economy: hard currency shortages, monetary duality, segmented markets, poor performance of the sugar and agriculture industries, inefficiency of public institutions, and distortions in the relative pricing system due to an overvalued official exchange rate and to a lack of convertibility. President Raúl Castro has publicly commented about these problems on numerous occasions.3

At the sector level, there are positive results in some areas such as oil and gas extraction. Oil production has increased six times since 1990 and gas production, which was negligible in 1990, now reaches over one million cubic meters. This allowed Cuba to reduce the volume of oil imports at a time when international prices are soaring. In addition, the petroleum agreement with Venezuela dampens the inflationary spiral for the crude Cuba buys; through ALBA the island receives low interest, long-term credit.

Overall manufacturing output has consistently decreased, accounting for 13.3% of the GDP in 2008. But performance varies notably by industry type. Nickel, beverages and liquor, tobacco and others grew, while the sugar industry has collapsed. Harvests are less than 15% of what they were in the early 90s.

Sugar cane yields dropped to only one million tons in 2008, owing to a drastic reduction in the availability of necessary inputs, the lack of incentives for producers and growers, and the low priority given to the sector in the 90s. This divestment had a negative impact on cultivation, yield and production, resulting in a significant reduction in exports and hence a major decrease in revenue and a disruption in financial flows into the national economy. In addition, half of the sugar factories in the country were closed. This downsizing meant solving the complex problem of retraining 100,000 newly unemployed workers. An extensive program was implemented, but it will not continue indefinitely, so workers will have to look for new employment in the medium term.

Agricultural production and farmers’ markets are important to the population’s food consumption and thus to its well-being. Agricultural production has continued to decline in recent years, accounting for less than 4% of the GDP in 2008, due to the aforementioned sharp decline in cane production, a continued decline in the livestock industry, and the stagnation of non-sugar crop cultivation. While acknowledging the reality of tangible problems, including shortages of financial and material resources, we must recognize that organizational and institutional problems have had a significant negative impact on economic performance in these areas.

The economic reforms of the 1990s enabled some State agricultural enterprises to be grouped into somewhat more flexible Basic Units of Cooperative Production (Unidades Básicas de Producción Cooperativa), but the highly centralized environment in which they functioned discouraged producers and impeded any increase in yields or production. The availability of external supplies was inadequate and the State procurement and distribution enterprise, Acopio, set such low prices for agricultural products that they were sometimes below the cost of production. Figure 4 shows that the decline in the production of starch crops (potato, sweet potato, cassava, plantains, etc.) and vegetables (tomato, cabbage, lettuce, onion, etc.) – essential in the Cuban diet – came at a time of runaway food prices worldwide.

Animal production has also been greatly affected by declines in the cattle industry caused by droughts in the eastern provinces, inadequate herd management and organizational problems. In addition, the cattle industry has had to practically abandon its heavy dependence on imported feed and on feed from the sugar harvests.

Animal production has also been greatly affected by declines in the cattle industry caused by droughts in the eastern provinces, inadequate herd management and organizational problems. In addition, the cattle industry has had to practically abandon its heavy dependence on imported feed and on feed from the sugar harvests.

The agricultural sector’s poor performance weighed heavily upon the country’s budgetary and trade deficits as large increases in food imports were necessary to ensure a daily consumption of 3,209 kcal and 88 grams of protein per capita in 2008 (although these figures remained higher than in 1989). Low levels of agricultural production and the resulting increase of food imports in an environment of rising commodity prices has made it necessary to reconsider the country’s agricultural strategy and policy, in search of development that is appropriate to the situation and new ways to unleash the potential of the labor force. Some changes of agricultural policy were made in the first half of 2008. Among other measures, an incipient market for agricultural inputs was established, land and livestock have been provided to private producers, and municipal enterprises have been strengthened, which is to say that the verticality of decision-making has been reduced.

Construction has increased enormously in recent years. For example, growth in the sector was 37.7% in 2006, concentrated in the areas of petroleum, electricity, tourism infrastructure and in the projects prioritized by the government as part of what is known as the “Battle of Ideas.” By 2007, however, new construction decreased as investments contracted due to a discrepancy between the resources allocated to projects and the capacity to carry them out.

Although substantial resources were invested in the 1970s and 1980s to expand the supply of housing, the housing deficit was still acknowledged to be a problem in 1989, and the crisis of the 1990s contributed to the further deterioration of existing housing. Since 2001 there has been a sharp drop in housing construction as resources were allocated to the recovery of housing damaged by multiple hurricanes and to other priorities. It has been clearly demonstrated that the construction of new housing will not by itself resolve the housing issue. Resources must also be allocated for the maintenance of the existing housing stock in Cuba. The state therefore accorded increased priority to the housing-construction in 2006 to combat the deterioration of existing housing and the housing deficit that had accumulated over decades. A program was established for the construction of 100,000 housing units annually, emphasizing self-building rather than State housing development. The program has many deficiencies (shortage of construction materials, lack of qualified personnel, difficulties with architectural designs, etc.) that must be solved right away, since the program only reached its goal in 2006, and in 2008 only built half the number of units intended.

Problems with public transportation have had a negative influence on the well-being of the Cuban population. Insufficient capital formation in the sector led to a rapid deterioration of equipment. A large-scale investment program outlined in 2007 permitted the importation of buses and other vehicles from the People's Republic of China, leading to major improvements in 2008.

In summary, Cuba's GDP growth trend continues, but it is still insufficient to regain the pre-crisis living standards of the 80s because of the structure of that growth. This means that new economic policies are needed to stimulate domestic activity and achieve greater production along with macroeconomic stability so as to meet goals of basic services and social equity.

Since 2008, there have been signs of a political will to make Cuban socialism more viable. Evidence of this has come in the form of removing some restrictions. For example, the sale of computers, DVD players and cell phones to Cubans has been authorized. Before, these were restricted to companies, diplomats and other resident foreigners. Restrictions on Cubans staying in tourist hotels were also lifted. Resolution 9 of the Ministry of Labor and Social Security allowed State enterprises to independently set employee wages, based on individual performance. Previously wages were set by the central government. Decree Law No. 259 turned over idle land in usufruct to individuals and cooperatives and shifted management of the agricultural sector toward non-State actors. Of the reforms implemented thus far, this one has the most structural significance.

3. External sector

The customary current accounts deficit in Cuba’s balance of payments continues today, despite some positive changes. For example, in 2005 Cuba enjoyed a surplus of over US$140 million due to increased export of medical services (especially to Venezuela), export of nickel, and the receipt of remittances widely estimated at between US$900 million and US$1 billion annually. But Cuba’s temporarily increased import capacity did not especially favor the import of capital goods (except for electrical generators); instead imports remain focused on food (much of which could be produced domestically) and intermediate goods.

Before the global crisis hit, Cuba’s nickel exports, unlike its sugar exports, increased in both unit-price and total amount. Foreign sales of nontraditional high-value-added products have also increased, including in the areas of biotechnology, pharmaceuticals, and advanced medical and diagnostic equipment. New markets have been found for these products. Nickel continued to be Cuba’s most important export in 2008 due to high prices on the international market. The export of pharmaceutical and biotechnology products also took off. The current structure of export products indicates a significant transformation. Medicines have been the third most important export subsector, while the sugar subsector has become less important. Nonetheless, sugar remains one of the products for which Cuba has the most productive potential.

Food purchases remain high because of inadequate agricultural production, and imports of equipment and raw materials for economic recovery have increased. This has led to a fairly substantial trade deficit of around 10 billion [convertible] pesos, which may lessen with increased domestic production of some currently imported items. But for this to happen, the Cuban government must give top priority to providing incentives for workers, while also implementing necessary institutional changes and eliminating over-centralization.

The recovery in the export sector is undeniable, but the value of exports in 2008 was still 31% less than in 1989. In contrast, imports have grown rapidly, exceeding their 1987 levels by 75% in 2008.

In 2008 Cuba’s main trading partners were Venezuela, China, Canada, Spain, and the United States (for imports of food), along with some European countries. This represents a structural change, in terms of composition by region, in comparison to the early 1990s. The service sector became the greatest generator of export income starting in 2004, but with significant qualitative changes as the value of knowledge-intensive services overtook the value of the tourist sector in generating income.

Income from tourism exceeded US$27 billion in the period from 1990 to 2008, growing from US$243 million in 1990 to US$2.36 billion in 2008. More than US$7 billion was spent on tourist development during that period. Of that amount, more than US$2.3 billion was spent on tourist infrastructure, airport capacity, and new technology for tourist services and telecommunications. Some 26 million people visited the country during that same period, and the number of hotel rooms increased from 12,900 in 1990 to 47,000 in 2009, nearly half of them managed by international hotel companies.

Foreign investment has been concentrated in key sectors such as petroleum, nickel, telecommunications, and tourism. International investment by Cuba has appeared in incipient form, primarily in biotechnology in Asian markets such as China, India, and Malaysia. At the same time, Venezuelan investment in the Cuban economy has increased.

Although balance of payments data for 2008 and 2009 have not yet been published, it is reasonable to anticipate a worsening of the balance of payments in these years. The current account of the balance of payments has been under deficit pressure from increasing interest payments on the growing foreign debt and from rising imports that are significantly overshadowing export growth. Substantial deterioration in the terms of trade has been decisive. The average price of nickel has fallen while the average price of food and fuel that Cuba imports has risen. This has caused a heavy strain on the stability of the international balance of payments, resulting in payment postponements and defaults and a growing foreign debt.

Professor Carmelo Mesa-Lago notes that foreign debt was US$18.3 billion in 2008 (54% active and 46% "immobilized" or unpaid for years), three times the debt of 1989. That is excluding the debt to Russia – estimated at US$21 billion – but including the debt to Venezuela, estimated at between US$5 billion and US$8 billion. The total debt, including non-convertible debt with former socialist countries, is estimated at US$45.9 billion. The foreign currency debt alone amounted to 380% of exports, in contrast to the regional average of 83% in 2006. Moody's rates the Cuban debt as "speculative and poor." Citing the rise in oil and food prices, Cuba suspended payments to Canada, Japan, Germany and France and also reported delays in payments for lack of cash. This increases the risk of a general default, diminishes the country’s financial credibility, and restricts access to new credit in the international market.4

The global crisis spread to Cuba in 2009, exerting added pressure on the balance of payments and affecting payment systems and banking operations. The excess demand for hard currency has caused a considerable delay in bank transfers, and in turn, has created more pressure on bank balance sheets, already affected by liquidity constraints imposed by the international financial crisis.

To deal with the hard currency deficit, Cuban economists have thus far reviewed the business plans of State enterprises, reduced by half the foreign travel budgets of ministers, reduced and suspended imports to certain sectors, postponed investments, decreased other budgeted expenses and limited cash withdrawals from bank accounts by foreigners. More recently, the emphasis has been on reducing and controlling energy use by institutions. The State sector has drastically reduced its electricity use, which accounted for the consumption of approximately 50% of imported fuel. Officials argue that not taking these measures would compromise the ability to buy food and medicine.

4. Macroeconomic Stability 4.1 Inflation

Since 1989, inflation in Cuba has gone through different stages. In the early 1990s hyperinflation hit mostly the informal market, since the state kept official prices frozen. The years with the steepest price increases in that market were 1991, with more than a 150% increase, and 1993, with more than 200% increase. The inflation was the result of the economic crisis, the economic policy adopted in order to tackle it, and the related fiscal and monetary imbalances. From 1990 to 1994, GDP contracted by 34.8%. The budget maintained expenditures for education and health, and subsidies to State-run enterprises grew in order to sustain employment. The average fiscal deficit from 1990 to 1993 was 24.9% of GDP.

Given the country’s limited capacity to access the international financial market and the lack of a public debt market, the fiscal deficit was financed by a loan from the Central Bank (at that time the National Bank) to the State budget. The monetization of the fiscal deficit led to an increase in monetary liquidity and a high rate of inflation in the informal markets.

A result seldom mentioned is the control of inflation achieved through economic policy since 1995. However, in a context of monetary instability it would have been impossible, for example, to maintain savings accounts in Cuban pesos open to foreign investment or to de-dollarize the economy as occurred in 2003 and 2004.5 In general, it would have been rather difficult to improve economic growth. The monetary stability created by monetary policy has decisively contributed to economic recovery.

Since 1995 the National Office of Statistics (ONE) has been drawing up a Consumer Price Index (CPI) listing average prices for the three markets throughout the country. The formal market registers the prices of rationed or non-rationed goods and services offered by the State to the public and represents 40% of the total CPI. The other two are the agricultural market and the informal market, each making up about 30% of the CPI. This CPI does not include, for the time being, the prices at markets in convertible pesos.

The evolution of this indicator is seen in figure 6. The Preliminary Overview of the Cuban economy by CEPAL (the UN Economic Commission for Latin America) reported that in 2008, the inflation rate accelerated to 4.9%, in comparison to 2.8% in 2007. One can see that inflation has not been high since 1995; in fact in some years there have been declines in average prices. Recently there has been strong pressure to raise prices, with five consecutive increases of more than 2%. But even so, as an average it remains within the range of what is accepted internationally as low inflation.

4.2 Balances and Monetary Policy

Table 1 shows the recovery of monetary and fiscal equilibrium beginning in 1995, following the hyperinflation of the 1990-93 period. In order to stabilize prices, it was necessary to decrease the fiscal deficit and maintain it at an average level of 3% of GDP. This reduced the amount of money in the hands of the people (the monetary aggregate M2A measures the value of cash and savings accounts held by individuals) and then monitored its increase. The exchange rate for the Cuban peso was revalued and has been stable since.

In order to recover monetary stability, a package of measures known as “Financial reorganization measures” was applied in 1994, which included charging for services that were previously free, increasing certain prices of products sold by the State to the population (mainly alcoholic beverages and cigarettes), and establishing various taxes and fees. Other parallel actions were taken that also contributed to monetary stability, such as partial dollarization, the opening of agricultural markets and facilities to receive remittances, expansion of self-employment, industrial downsizing, the development of tourism and foreign investment, etc. In 1994 the convertible peso was also created and pegged to the US dollar. This currency operated marginally in the retail market for approximately 10 years until in 2003 and 2004 its use was expanded as part of the de-dollarization of the economy.

Monetary policy was strengthened with the creation of the Central Bank of Cuba and its Monetary Policy Committee, which systematically analyzes the variables linked to monetary equilibrium and that have an impact on inflation. The exchange rate of the Cuban peso in official currency exchanges (Cadeca) is set by the Monetary Policy Committee, but it is based on the public’s currency-trading activities at the exchange houses. So ultimately the exchange rate is determined by the currency demand pressures generated by wage and other income sources in Cuban pesos and the supply of foreign exchange generated by tourism, remittances, etc. Farmer’s markets, stores run by MINCIN (Ministry in charge of State-owned retail stores in Cuban Pesos), and self employment are also influential, since they increase the demand for Cuban pesos. In addition, the buying-selling of currencies is affected by the expectations and confidence of the population regarding the different currencies.

The Central Bank has also employed another tool. It adjusts the interest rate in order to maintain monetary equilibrium for the population. The Monetary Policy Committee fixes interest rates on bank deposits in the three currencies for all banks comprising the Cuban financial system. Table 2 shows the rates for the different currencies at the close of 2008.

The interest rate increase in Cuban pesos and the favorable differential that has sustained the interest rate of national currencies in relation to deposits in dollars has helped to encourage savings in the national currencies, and therefore, has also helped to stabilize official currency exchanges and the exchange rate. In addition, it has served to reduce consumption demands and therefore price pressures.

Although not all Cubans have savings accounts, from the macroeconomic standpoint and for monetary stability, savings activities themselves are very important. Typically around half of the liquidity of the population remains in the form of savings in banks. Therefore, the decisions made by savers have a significant effect on the stability of exchange rates and prices.

Along with the Monetary Policy Committee and its instruments, the role of the Organization of Internal Finances Analysis Group (Grupo de Análisis del Saneamiento de las Finanzas Internas, GASFI) in assuring monetary stability should be highlighted. The heads of the Ministry of Economy and Planning, the Ministry of Finances and Prices, MINCIN, and the Central Bank meet every month in the GASFI to plan the actions each one should take to maintain monetary equilibrium in the population. This is where monetary policy, fiscal policy and planning meet. All this planning and organization of monetary policy has served to maintain monetary equilibrium since 1995. Nevertheless, in 2008 inflation climbed, causing a dangerous 6.7% increase in the fiscal deficit, the highest in 14 years. In 2009, the global crisis and other internal factors have continued exerting pressure on monetary stability and have even impacted Cuban Banks. If this continues, monetary and financial stability could return to being among the principal objectives of the country’s economic policy.

5. Personal incomes

5.1 The real wage

Table 3 presents an estimate of the real wage, offering a quantitative look at one of the most talked about events in the Cuban economy: the crisis of the 1990s. The drop in the purchasing power of workers’ wages in State-run enterprises and institutions, and its continued low level, has caused a lack of incentive, emigration of skilled labor, and illegal activities, among other distortions.

The annual inflation rate is expressed cumulatively in column B of Table 3, from 1990 to the present, with the result that a Cuban peso in 1989 is equivalent to 9.25 pesos today. The mean nominal wage is located in column C, which in 2008 was 414 Cuban pesos, more than double the 1989 value (188 Cuban pesos). In the last column, the nominal wage (C) is divided by the price-level (B), to give the real value of the mean wage measured in 1989 pesos. A gradual recovery can be discerned in the real wage starting in the mid-1990s, although it is still very far from pre-crisis levels. At the close of 2008, the real wage was equal to 45 Cuban pesos, that is, 24% of what it was in 1989.

When comparing column A to B, one can see the difference between inflation and price levels; inflation is low starting in 1995, but the price levels are much higher than before the crisis due to the hyperinflation of the early 1990s. Table 3 distinguishes monetary stability from purchasing power and helps to focus the discussions of prices and wages on a single concept that sums up both things: the real wage. Estimates of the real wage show the need of Cuban families to resort to other income sources in order to cope with the impact of the crisis.

The calculations in Table 3 are not exact, but are estimates, since there are no official data on inflation before 1995. Nevertheless, the trend of real wages is confirmed by other estimates of the CPI made in the 1990-94 period.

To measure the purchasing power of the real wage in Cuba it is common to divide it by the exchange rate used in the official currency exchanges and then express the wage in US dollars. This method leaves out the subsidies, free services and other benefits that the Cuban government offers the population and which are not included in the wage. This makes international comparison difficult. The calculation of the real wage is a less biased approach because it compares different moments in time during in which subsidies and gratuities have existed. Curently, a higher proportion of basic goods has to be obtained from unsubsidized markets; therefore the decline in the population’s purchasing power is greater than suggested by examining only the wage-trend.

5.2 The ration card

The deterioration of the real wage did not bring dire poverty to Cuban families, since important social expenditures and subsidies, including the ration card were maintained. Today one can see progress in macroeconomic conditions: certain production sectors have recovered, trade and financial relations with other countries have been re-established, and the GDP has grown. In this context, the possibility of doing away with the ration card has been discussed. Given the low level of the real wage, this evidently cannot mean the elimination of the subsidies related to the ration card, but rather a change in the way they are made available.

The domestic food market is highly segmented. Analyzing the ration card system could be a step toward unifying the various food markets into just one. It has been pointed out that the ration-card food distribution system stopped fulfilling its original purpose, which was to ensure equity, some time ago. At present it subsidizes equally those who need it and those who do not. This method of distribution does not favor or encourage growth in productivity, as some people simply adapt to it.

Nor does this form of distribution provide alternatives to the consumer, who has to buy the goods at a set location with a limited supply of items. Actually, the amounts and composition of rationed products today are rather far from those initially supplied on the ration card when it was established (1962). At current levels of food consumption, rationed distribution covers the needs of approximately 12 days per month. More specifically, the ration card covers 10 days worth of protein and 9 days worth of fat per month.

The ration card is a way to assist people through providing an allotment of foodstuffs at subsidized prices, ensuring that no individual or family that needs aid is left outside of the rationing system. However, it is not cost effective to the extent that it assists families who, given their level of income, do not need such subsidies.

An alternative is to not subsidize products but rather directly help low-income families. Not subsidizing the families with higher incomes would lead to savings and an improved capacity to aid those with scarce resources. In this way, eliminating the ration card would result in an increase of resources per capita for assigned subsidies. There is the obvious risk of a needy citizen being left out. The challenge lies in being able to identify the low-income and high-income families, and create a fair dividing line between them.

6. Principal Challenges

The Cuban economy faces many complex challenges to maintaining its social and economic project and retaining the capacity to increase the well-being of the population. Social and economic distortions must be confronted, and time is short.

- Internal factors that continue to constrain economic growth must be overcome in the short to medium term. Among them are shortages of hard currency, causing consumer needs to go unmet.

- State enterprises are currently subject to an adverse environment that includes problems related to price setting, the official exchange rate, the framework of exchange regulations, the centralized authorization of purchases, and other planning, regulation, and auditing mechanisms. Enterprises must achieve a level of efficiency sufficient to be competitive on the international market.

- The so-called income/consumption model is still seriously distorted as evidenced by its effects on labor motivation. Labor compensation systems must be made coherent in order to resolve problems in satisfying the needs of workers through salaries, other forms of income, or redistributive channels. This model’s effect on market segmentation and the availability of goods and services must also be addressed.

- The restructuring of the sugar industry remains incomplete, and therefore the recovery of production in the industry has stalled, also affecting the production of food on land ceded to growers for this purpose by the Sugar Ministry (MINAZ).

- There has been no progress toward achieving food self-sufficiency through improvement of the model of agricultural management.

- Greater short-term priority should be placed on addressing the decapitalization of infrastructure and equipment, given the cumulative effects of their deterioration.

- Cuba’s production specialization must be changed radically, from an economy based on exploitation of natural resources to one based on the intensive use of knowledge. Cuba’s strong potential in knowledge-intensive development does not by itself guarantee positive outcomes.

- The strategic challenge is to grow, as other benefits derive from growth. However, new springboards must be found to increase production. Performance is declining in sectors and activities such as tourism that have been used to increase production in the past.

- Measures should be accelerated to recover previous levels of social equity. Despite progress in recent years with measures such as the distribution of household appliances associated with the Energy Revolution,6 the problem of family income has not been resolved satisfactorily for the majority of Cuban families. Part of the population is still unable to cover all their expenses with the incomes they receive from the formal sector. As a result they have to seek income from alternative sources or do without a series of goods and/or services.

- While Cuba is an advanced country as measured by social indicators concerning health, education, culture, and other areas, access to certain goods and services in areas including recreation, travel, transportation, and communication is far below the world average for comparable countries.

- It is necessary to consider devaluation of the official exchange rate and the creation of an exchange mechanism for the Cuban peso in institutions as part of the process to eliminate the double currency, replace the ration card by another system of subsidies that is more efficient and has better distributive results, and make institutional changes that would lead to fewer ministries and less centralization in the public sector.

- Cuba reaped substantial benefits from its relationship with Venezuela in the 2004-07 period. Nevertheless, the relationship has additional untapped potential to develop reindustrialization programs that would complement and support new dynamic sectors and allow for the recovery and expansion of sectors that are strategic in light of their impact on the quality of life of the population and on the export sector.

- Cuban State enterprises have not taken on innovation as one of their basic tasks. Not only does the economic system suffer from functional deficiencies but it has led to a kind of dead end, unless there is a substantial transformation.7

Conclusions

The Cuban economy enjoyed an expansive cycle from 2004 to 2007 that was closely linked to agreements with Venezuela and the export of professional services. During that period the importance of services to the total GDP increased, reaching 76%, while agriculture, industry and tourism stagnated. The deficit between imports and exports of goods rose. A shift in trade relations, with Venezuela and China predominating, was accompanied by an increase in foreign debt and fewer foreign companies operating on the island. At the same time, inflation was controlled and in general fiscal equilibrium was maintained. However, the real wage remained extraordinarily low.

Since 2008, a reverse process has begun, with a slowdown exacerbated by the global crisis but also caused by external imbalances and structural weaknesses that were left unresolved during the period of expansion. The new government of Raúl Castro has implemented a set of changes and has oriented economic policy priorities toward import substitution, increased agricultural production, control of energy expenditure, and diversification of foreign trade and financial relations. However, the steps taken so far are only a small fraction of those needed to address the structural challenges to the island’s economy and significantly increase the purchasing power of the Cuban family.

There is a growing consensus regarding the need to debate and further transform the Cuban economic model, which essentially still looks like the Soviet model based on state ownership of most of the economy, wage labor and centralized resource allocation and price determination. Adherence to this model has been independent of the existence of the US blockade, which intensifies to an extreme the external constraints on Cuba’s economic growth.

The structural challenges must be solved by changing the management mechanisms of State enterprises, enabling greater employee participation and greater autonomy for managers to make decisions and set prices. In addition to transforming the inner workings of State enterprises, their economic environment must change too, giving the market and competition a greater role.

Along with this crucial transformation, more opportunities for non-State forms of ownership must be provided. Cooperative ownership should be allowed in the services sector and small industry. Foreign investment should be facilitated and expanded to areas currently off limits such as the sugar industry. The failure of "real socialism" in Eastern Europe and the continued inefficiency and vulnerability of the Cuban economy should prompt radical changes in the economic model without giving up its social benefits.

Bibliography Anuario Estadístico de Cuba, Oficina Nacional de Estadísticas. Havana: various years. Banco Central de Cuba. Informe Económico, Havana: 1997, 1999 and 2001.

Castro Díaz-Balart, Fidel, Ciencia, Tecnología y Sociedad, Havana: Editora Política, 2001.

Centro de Estudios de Economía Cubana (CEEC). “La economía cubana en 1996: Resultados, Problemas y Perspectivas” Havana: Universidad de la Habana, 1997.

CEPAL, Balance preliminar de las economías de América Latina y el Caribe. Santiago de Chile, 2004.

CEPAL, “La economía cubana. Reformas estructurales y desempeño en los noventa.” México: Fondo de Cultura Económica, 1997.

Ferriol, Angela, Maribel Ramos and Lía Añé. “¿Pobreza en la capital?” Havana: INIE-CEPDE/ONE, 2004.

García Álvarez, Anicia and Viviana Togores González. El acceso al consumo en Cuba y su repercusión en la vida cotidiana. CEEC, 2002.

Iñiguez Rojas, Luisa. “Desigualdades espaciales en Cuba: Entre herencias y emergencias.” Centro de Estudio de Salud y Bienestar Humanos. University of Havana, 2004

Martín Fernández, Mariana and Ricardo Torres Pérez. “La economía del conocimiento. Evolución de las tendencias mundiales y experiencias para Cuba.” Thesis, Facultad de Economía, University of Havana, 2004.

Ministerio de Finanzas y Precios. 1998. Resultados de las medidas de saneamiento financiero aprobadas por la Asamblea Nacional del Poder Popular. Havana.

Monreal, Pedro. “El problema económico de Cuba.” Espacio Laical (publication of the Archdiosis of Havana), no. 28, April, 2008.

Nova González, Armando. “Redimensionamiento y diversificación de la agroindustria azucarera cubana. CD, Evento 15 años del CEEC, Havana: May 2004.

Pérez, Omar Everleny. “Cuba’s Economic Reforms: An Overview,” Special Studies No 30, Perspectives on Cuban Economic Reforms, eds. Jorge F Pérez López and Matías Travieso-Diaz, Center for Latin American Studies Press, Arizona State University. 1998.

Pérez, Omar Everleny. “Reflexiones sobre economía cubana” Havana: Editorial Ciencias Sociales, 2007.

Triana Cordoví, Juan. “El desempeño económico en el 2002” in 8vo Seminario Anual de la Economía Cubana, CEEC, CD version, Havana, March 2003. Vidal, Pavel and Annia Fundora. “Relación Comercio-Crecimiento en Cuba: Estimación con el Filtro de Kalman” Revista de la CEPAL 94. United Nations. April 2008 Vidal, Pavel. “La Encrucijada de la Dualidad Monetaria,” Nueva Sociedad. July-Aug 2008.

Xalma, Cristina. “La dolarización cubana como instrumento de intervención económica. Eficacia y sostenibilidad de una alternativa.” Doctoral Thesis, Barcelona, September 2002.

Notes

1. The new method of calculating GDP gives greater weight to the social services that before were only valued at cost, since they are provided for free. Since 2004, “artificial” fees were established for use in GDP calculation. There is debate, including within the UN Economic Commission on Latin America (CEPAL), about the validity of this method and its implications for comparing the Cuban GDP internationally.

2. The significant role of exports in Cuba’s GDP is empirically demonstrated in Vidal & Fundora 2008.

3. Speeches by Raul Castro: July 26, 2007, in the province of Camaguey and February 24, 2008 in the National Assembly of People’s Power, in Havana.

4. See Carmelo Mesa-Lago: “La economía cubana en 2008-2009: retos internos y externos, estado de las reformas y perspectivas,” presentation at the Seminar on Cuba in Costa Rica, 2008.

5. After 10 years of USD circulation in the economy, in 2003 current bank accounts of State enterprises changed to convertible pesos. In 2004 de-dollarization extended the use of convertible pesos to individual bank accounts and retail markets.

6. The Energy Revolution is an energy conservation program. It includes distributing electrical appliances, replacing incandescent by energy-saving light bulbs, improving energy production capacity via small, decentralized generation plants, and utilizing gas and renewable energy.

7. Pedro Monreal, “ El problema económico de Cuba. Espacio Laical,” publication of the Archdioses of Havana, April, 2008. No 28, Havana.